KMI is a energy company. I initiated a position a few months ago, needless to say the stock has shed a ton. I’m averaging down. I think oil companies might not have reach the bottom yet, as the Iran nuclear deal has running thought “smoothly”, us-Russia relation is restoring, there could be more Russian’s oil hitting the market? The Chinese growth has been slowing sending energy sector down by 20-70% from 52 weeks high.

So why am I picking KMI?

- High yield. Sitting at $27. It’s now yielding at 6.7%. Try to get that from a saving account.

- Averaging down. Once I take a position, I don’t sell. So, average down is probably the best way to reach back to breakeven point.

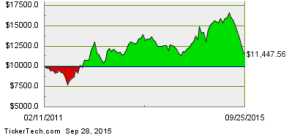

- The stock price is less than the post split price. yet, if you invest in 2011, you’d still improve by 17%. That has just showed me the power of dividend paying stock, you’d still be ahead even the stock has shed 50%. Pretty cool stuff.

- The company has 80,000 miles of pipelines for natural gas. This business just don’t stop even of the price drop.

- It operates a refinery business. Regardless, the oil price, the refinery cost is a fixed amount. So, they will still make a profit.

- Dividend aristocrats don’t cut dividend. They would rather cut cost, lay off employees, but they don’t stop paying dividend, don’t cut dividend, otherwise investors will lose trust, and the stock price will plummet like there is no tomorrow.

What’s about you? Have you make any buys lately?

Great purchase price for a great company. I love the toll road business model…cant get my hands on enough of KMI and similar business model companies.

Congrats on adding more to your dividend income!

R2R

It’s definitely boost my yield on cost. The dividend growth investment method didn’t click to me until I have to see it in action when other investors put out there. I can’t believe that these companies would rather cut cost by cutting the number of employees rather than cutting dividend. And they would do it for decades on out. DOV they do it for almost 60 years. I was super surprised by it. They survived the great recession 2008-2012. I think they’ll survive for many more years and continue to issue dividend like clock-work regardless how moody the market is.

What do you think about their large debt (KMI’s Debt/Equity of 126.67%)? Any risk for investors in the near term or long term that you perceive?

As far as I can tell, this debt to equity number is on the decline for KMI. I can’t add a picture here, I added it my analysis.

Great buy. I really want to add more KMI right now but my energy sector stocks are taking up too much of my portfolio. I like this purchase for you though.

I don’t have much energy, so I’m at liberty of adding more. By march next year, the energy should stabilize, as earning has come to a full cycle of down revenue. But I’ll keep watching for more deal in the future.

Great purchase Vivianne! I also added to my KMI position last month. As long as this energy sector downturn persists, I’ll continue to add to my energy holdings. As I don’t think “this time it’s different”. When commodity prices are going to recover, I can stop adding and continue to underweight my sector allocation by purchasing into other sectors only.

Thanks for sharing and good luck to you!

DivRider

Thank you for visiting and commenting. It’s great to be fellow shareholders.

Energy poses very attractive yield at this point. I have limited holding with good reasons. If the rate increases, the commodity price will drop. Metal sector will also be affected. That’s why I’m also into industrial like DE, CAT and EMR (even WMT is now asking supplier to reduce price on product due to falling material price).

Slowly adding energy sector is a better way to go, I’m looking to add energy at the first rate increase until the sector stabilize. I don’t want to buy and sell, at the same time, I don’t like seeing dividend cut after I buy a stock either. I want to see some sustainability in dividend payout and company cash position. KMI is pretty tight at the moment, we will see how it’s all going to pan out.